At Zeifmans, we’ve spent decades working closely with small business owners as they set goals for the future, create strategies to achieve them, and develop the infrastructure to maintain that wealth over the long-term. We pride ourselves on being innovative, continually striving to think outside the box and deliver solutions that give our clients the competitive edge they deserve.

The opportunity to secure funding for a new business endeavor, or simply to support further growth, represents a major milestone for many small businesses. But in securing a loan, there are myriad factors that influence whether or not that money will truly benefit the business, or result in a risk that’s greater than the benefit.

One such lending configuration that we are often asked about is the Interest Rate Swapping. Banks present this scenario as an option for clients seeking stability and cost savings for the future. And while an Interest Rate Swap isn’t the answer for everyone, it is an appealing option that’s worth considering for many reasons. Let’s take a closer look.

Interest Rate Swapping: A long-term alternative

In providing the option to engage in an interest swap scenario, banks promise a number of intriguing features:

– Improved contractual terms

– Customized financing that includes prepayment or extension options

– The ability to hedge interest rate exposure by locking in a fixed rate on a future-starting loan

– The ability to influence loan structure at market rates with two-way breakage costs

Banks combine a Bankers Acceptance (BA) Loan and an Interest Rate Swap in order to provide this cost effective and flexible option.

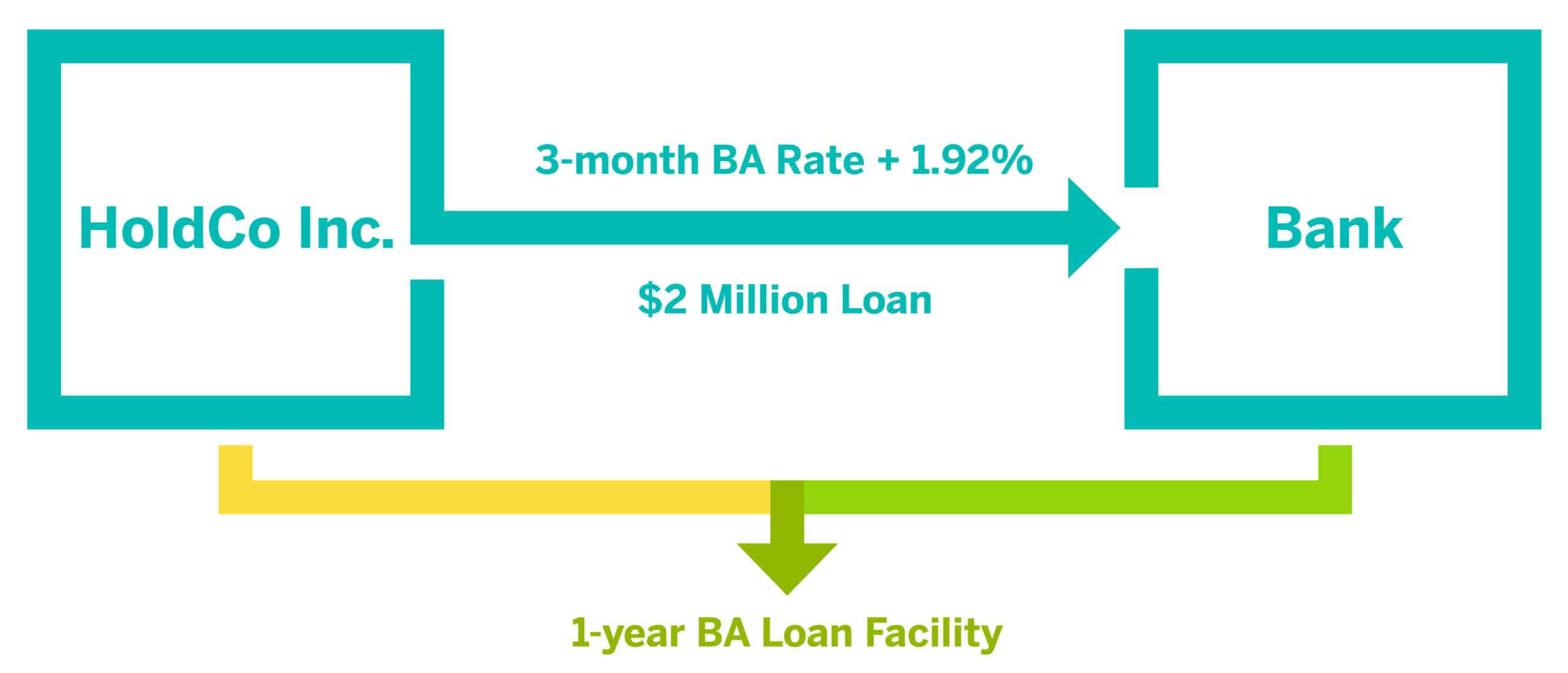

What is a BA loan?

A BA loan is a floating rate loan that has a rate of interest based on a market driven rate, plus a Credit Spread, as illustrated by the below example:

The BA loan provides the client with a floating rate. To fix the interest rate, the bank provides an Interest Rate Swap.

What is Interest Rate Swapping?

Interest Rate Swapping is a contract between a client and a bank, in which the two parties agree to exchange fixed rate payments for floating rate payments based on a pre-determined term and amount. Essentially, in a swap scenario, a floating rate is exchanged for a fixed rate.

For example, a client could achieve a 16-year fixed cost of funds on a BA loan facility if overlain with a 16-year Interest Rate Swap. Upon maturity, the bank assesses the credit spread and can adjust it higher or lower.

A traditional term loan product contains two underlying components: The spread that the lender is anticipating they will earn, and the cost of funds. By disaggregating these two components via an Interest Rate Swap, the client can achieve more flexibility, and lower costs.

Is an Interest Rate Swap right for your organization?

At Zeifmans, we seek first to gain an in-depth understanding of your business needs and goals. By putting relationships first, we’re able to offer so much more than traditional accounting services, using our expertise to act as trusted business advisors for many of our clients’ most important financial decisions.

If you’re considering options for future financing and are interested in exploring an Interest Rate Swap, contact our team today to gain more insight into how this option could work for you.

For a PDF copy of this article, click here.