For many Canadians, charitable giving isn’t just about taxes – it’s about making a difference. But changes to the Alternative Minimum Tax (AMT) might make generosity a little more complicated, especially for those making large donations. If you’re donating cash or marketable securities, understanding how these new rules work can help ensure your giving is as impactful for your community as it is for your financial plans.

At Zeifmans, we help people and businesses navigate these kinds of changes so they can focus on what matters most – whether that’s supporting their favorite cause or achieving their financial goals. Let’s break down the rules and what they mean for you:

What Is the AMT and Why Does It Matter?

The AMT is a backup tax system designed to ensure high-income earners pay a baseline amount of tax, even if they qualify for multiple credits and deductions. Essentially, the AMT asks: “What’s the least you can pay, given all the benefits you’re claiming?”

Under Bill C-69 (2024), the government introduced rules for calculating AMT, aiming to increase the proportion of taxes paid by wealthier Canadians.

Key Points:

- Capital gains inclusion rate: Now, 100% of your capital gains count toward your AMT base (up from 80%). However, for regular income tax purposes, the inclusion rate remains at 50% for individuals, as the previously proposed increase to 66.67% was officially cancelled in 2025

- Donated securities: If you donate qualifying securities, 30% of the associated capital gain is now included in your AMT base (donated securities still have AMT inclusion implications).

- Donation tax credit: You can now only apply 80% of your donation tax credit to reduce your AMT (down from 100%).

- AMT rate increase: The federal AMT rate is now 20.5% (up from 15%).

- Exemption increase: The income threshold for AMT has risen to $181,440 for 2026.

These changes mainly target high-income taxpayers and those making substantial donations.

What Do These Changes Mean for Charitable Giving?

While giving to charity remains an incredibly impactful way to support causes close to your heart, the new AMT rules make the tax math trickier – especially for donations involving marketable securities.

Here’s a quick example:

- Under the old rules, if you donated shares with a $50,000 capital gain, none of that gain would have been added to your AMT income.

- Now, under the new rules, 30% of that $50,000 gain—or $15,000—must be included in your AMT calculation.

For high-income taxpayers, this could lead to higher taxes in the short term, even though AMT credits may help offset future tax liabilities.

Real-Life Scenarios: What Do the Numbers Look Like?

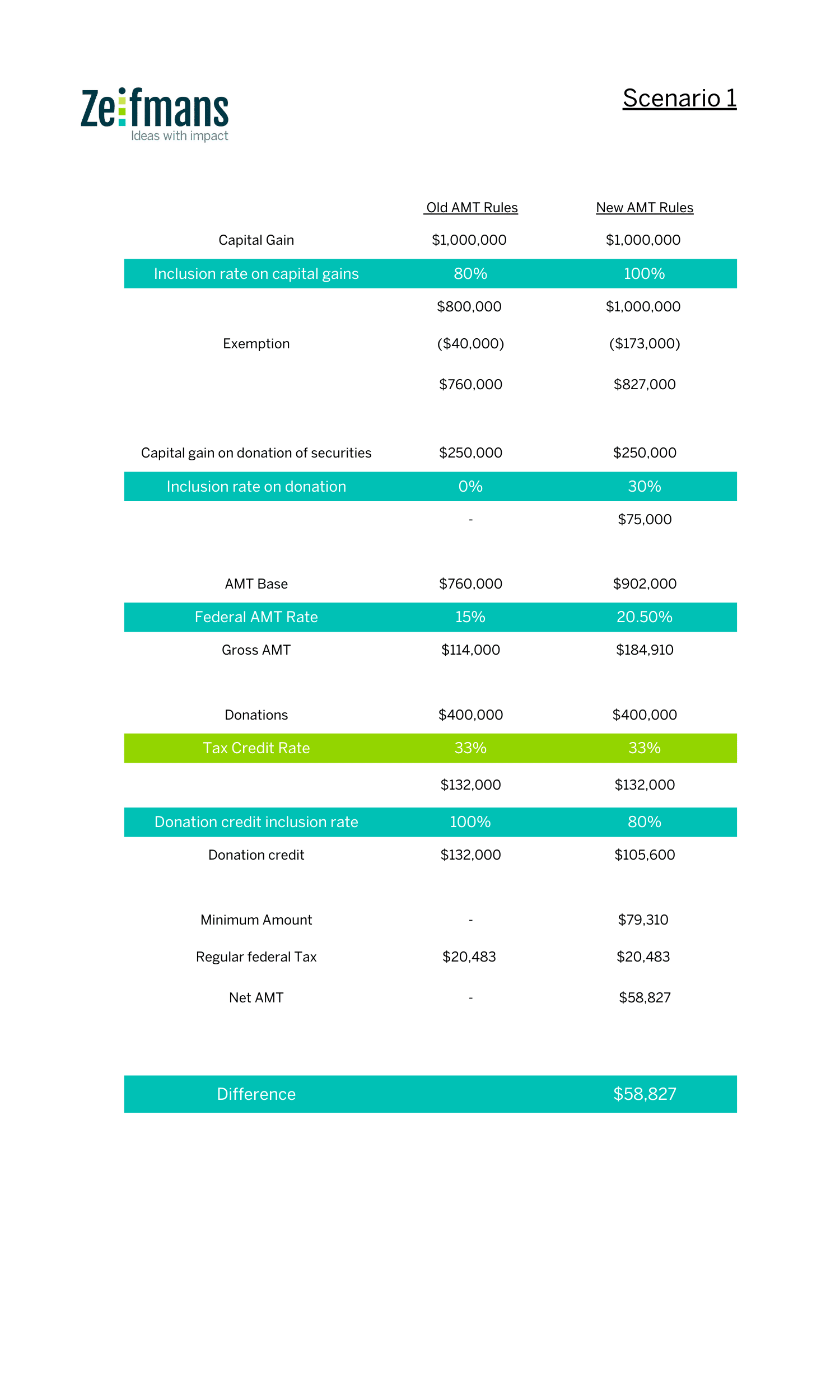

Scenario 1: Donating Securities

Let’s say Rachel, a Vancouver resident, sold publicly traded shares for a $1 million capital gain. She also donated additional shares worth $400,000 to a registered charity, which had an adjusted cost base of $150,000.

Scenario 1: Donating Securities

Let’s say Rachel, a Vancouver resident, sold publicly traded shares for a $1 million capital gain. She also donated additional shares worth $400,000 to a registered charity, which had an adjusted cost base of $150,000.

Under the new AMT rules:

- Rachel must include 100% of the $1 million gain from her sale in her AMT base.

- She must also include 30% of the $250,000 gain on the donated shares.

- Combined with the reduced 80% limit on donation tax credits, Rachel’s total taxes owed under AMT increased by roughly $58,827 compared to the old rules.

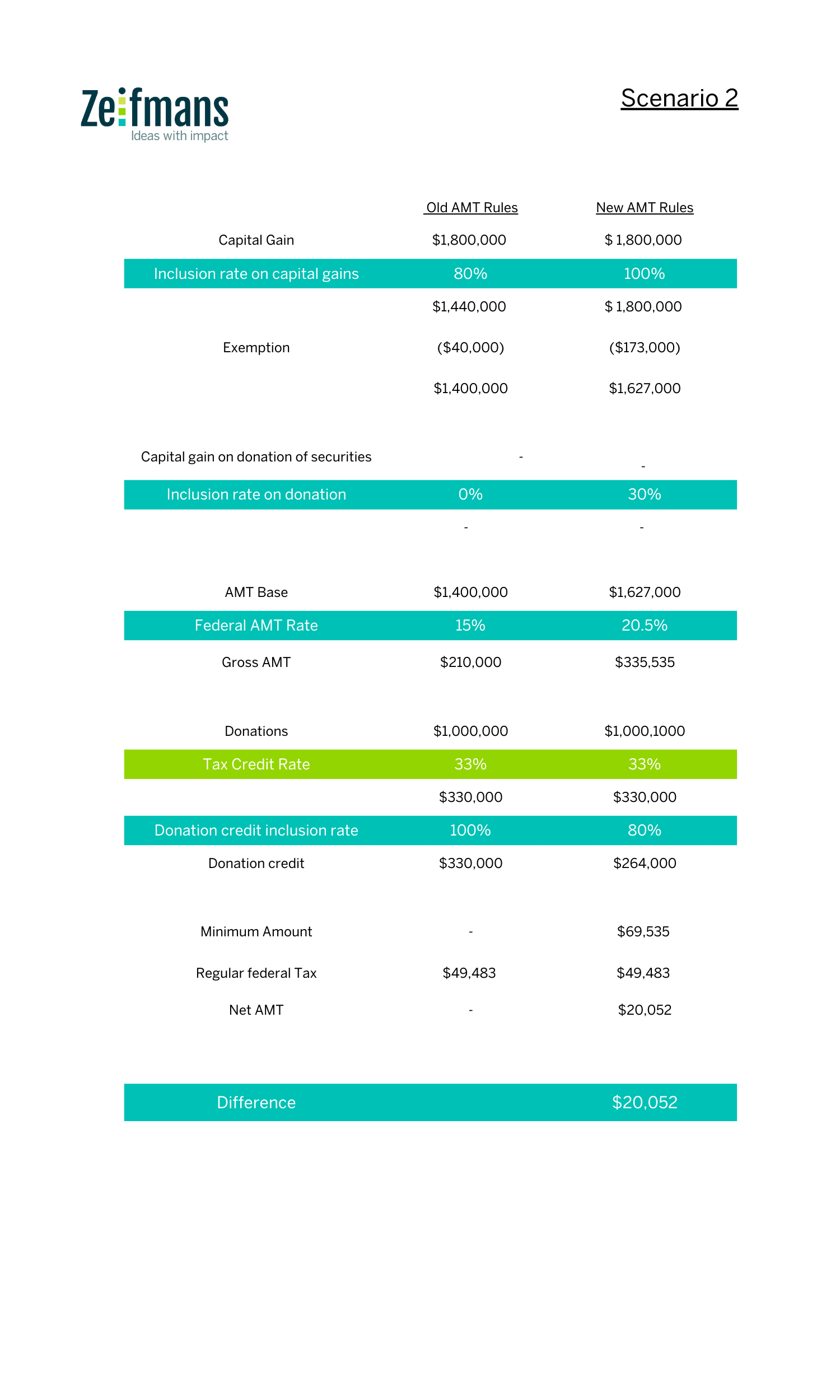

James, an Ontario resident, sold real estate for a $1.8 million capital gain and donated $1 million in cash to his favorite charity.

Under the new rules:

- James must include the entire $1.8 million gain in his AMT base.

- Since only 80% of his donation credit can reduce his AMT, his taxes increased because he can no longer utilize the full 100% of the credit to offset the AMT liability.

These examples show how large donations can trigger unintended tax consequences, making careful planning essential.

How to Manage the Rules

If the new AMT rules seem daunting, don’t worry – there are ways to plan around them. Here are some strategies:

- Plan donations strategically: Consider making donations through your will, as AMT doesn’t apply in the year of death.

- Model your tax impact: Work with a tax professional to calculate how much to donate and when, ensuring you don’t accidentally overcommit and increase your AMT base unnecessarily.

- Time your capital gains: Since the general capital gains inclusion rate remains at 50% for individuals, you have more flexibility in timing sales, though the 100% AMT inclusion remains a factor for high-income years.

- Use AMT carryovers: If you pay more under AMT now, you may be able to offset future taxes with AMT credits over the next seven years.

Keeping Generosity a Priority

The AMT rules are part of the government’s push to make the tax system fairer by asking wealthier individuals to contribute more. But they also create additional hurdles for those who want to give generously.

With the right planning, you can still make meaningful contributions to the causes you care about while minimizing unintended tax consequences. At Zeifmans, we’re here to help you strike that balance, so your generosity has maximum impact – both for your community and your financial goals.

If you’re considering a large donation or want to explore your options, reach out to Zeifmans today. Let’s make your giving as effective as it is meaningful.

{kind=link}

{kind=link}